The construction and engineering sector is having a moment—and it's not subtle. In Q3 alone, deal value surged to $36.7 billion, a 34% leap from the previous quarter.

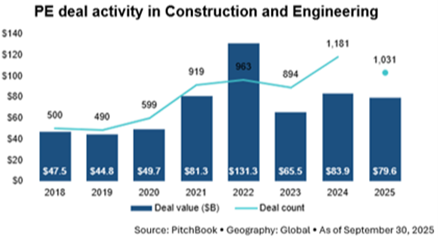

Fewer deals closed, but they were bigger, bolder and more strategic. Over the first nine months of the year, deal count rose 14% year-over-year, and total value hit $79.6 billion, up 19%. That's serious momentum.

PE is clearly shifting gears. Investors are chasing scale, not just stacking small add-ons. Rising valuations may be making those smaller deals harder to land, but the appetite for consolidation is still strong.

Specialty construction, including HVAC, plumbing, electrical, interiors and facades, remains fragmented and full of potential. Elevated valuations may be making deals harder to close, but they are still happening; underlying demand is too compelling.

And then there's the data center boom. As AI and tech continue to explode, the need for infrastructure, especially electrification and cooling, is skyrocketing. PE firms are jumping in, seeing construction and engineering as the backbone of the digital future.

There's also a practical edge to this sector. It's relatively shielded from tariffs, thanks to its service-heavy revenue model. Even when material costs rise, many firms can pass those costs on to customers. Projects have long lead times, and revenue streams are highly visible.

Scale can add significant value, enabling bidding on increasingly larger projects. Add in the push for nearshoring and reshoring, and you've got a recipe for sustained demand in factories, warehouses and infrastructure.

Big deals are making headlines. KKR's $6.5 billion buyout of Spectris and Vista Energy's $2.0 billion acquisition of Acumatica are just two examples. On the exit side, activity mirrored the deal trend: fewer exits, but bigger ones. Exit value rose 14% to $33 billion, with Apollo Global Management's $2.3 billion acquisition of Kelvion and Blackstone's $1.6 billion purchase of Shermco Industries leading the pack. |